February 04, 2003

Stock Prices

While we have already discussed the most fundamental explanation for stock prices ("It is all a matter of supply and demand," reference),

we can also use present value calculations to think about the basis for that demand.

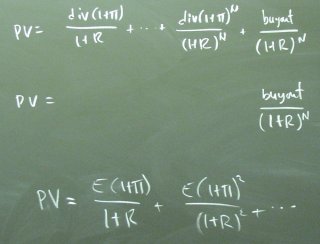

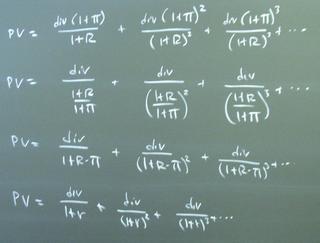

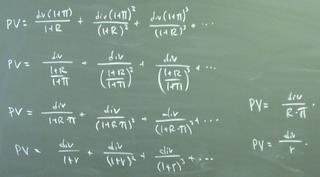

We derived two equations:

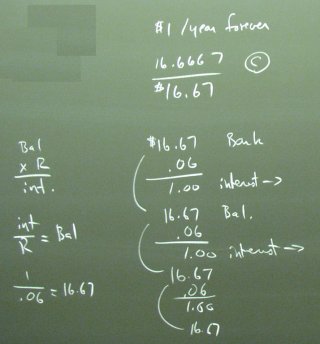

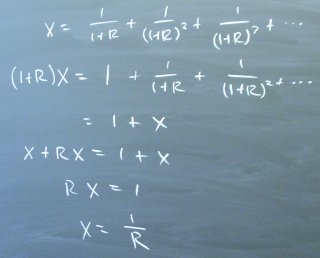

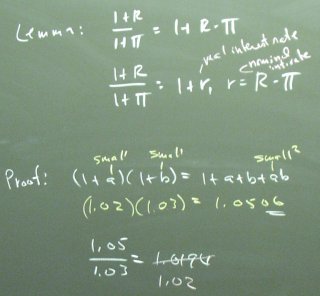

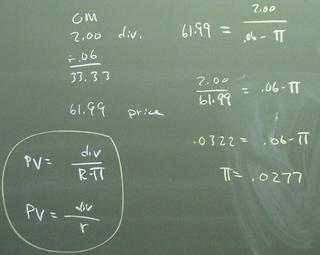

We first need to know that, if you discount at rate R, then one dollar per year forever is worth 1/R. We worked this out for R = 0.06.

Here is a little more mathematical view of this result.

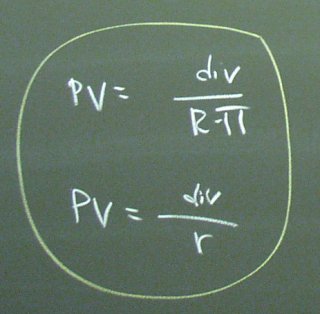

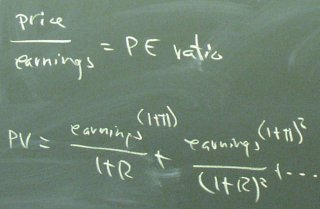

Suppose a stock pays a dividend that grows at rate pi.

The steps above use a fundamental lemma:

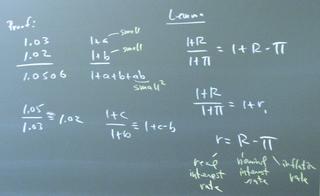

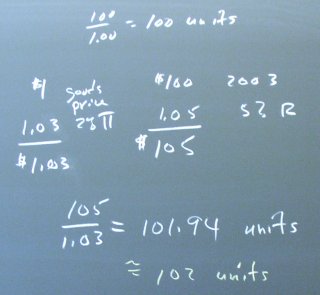

To think about real interest rates, we can consider getting 5% interest on a bank account while the good we consume is going up in price by 3%. Our real return is only 2%.

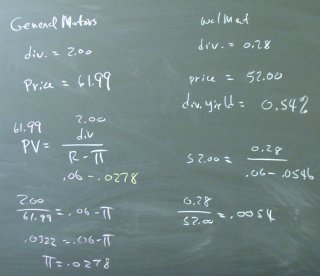

We then applied our new equations to General Motors, which has a $2 dividend, but a $62 share price. If the interest rate is 6%, the share price would be sensible if the expected dividend growth rate is 2.77%. Thus, a dividend yield of only 3.22% is not necessarily a sign that General Motors is a bad investment relative to 6% government bonds. WalMart has a dividend yield of 0.54%, which implies that people expect their dividends to grow at a rate of 5.46% per year.

People also might discount earnings instead of dividends. This makes sense if you think that retained earnings are valuable because they represent some kind of future return. The price-earnings ratio is upside-down relative to the dividend yield, but that is the way people think about stocks. It might make more sense to have the dividend yield and the earnings yield.

Finally, we accounted for Microsoft, Amazon, etc. that do not pay dividends by discussing share repurchases and the possibility of a "buyout" payoff in the future.