February 18, 2003

Duration

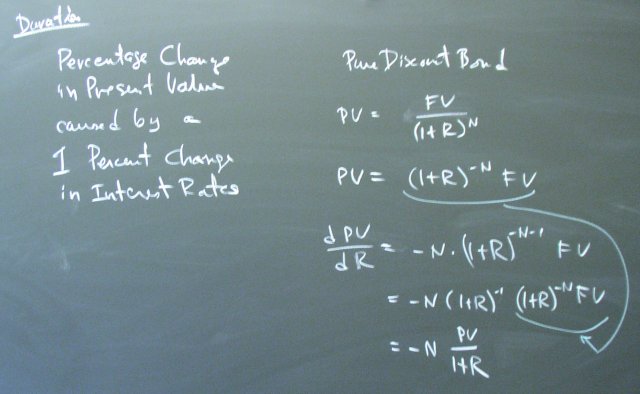

What is duration?

We can look at this as calculus or as "the rise over the run." The first derivative gives us a linear approximation to the nonlinear function in the graph.

You will find the average duration of a bond or mortgage portfolio used to talk about the degree of interest rate risk associated with that portfolio. A bond portfolio with a duration of 10 goes up or down about 10% in value when interest rates change by one percentage point, just like a 10-year pure discount bond.

Posted by bparke at February 18, 2003 01:01 PM