April 25, 2003

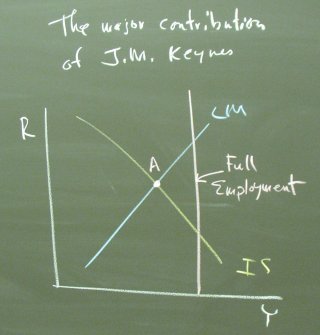

The Major Contribution of J.M. Keynes

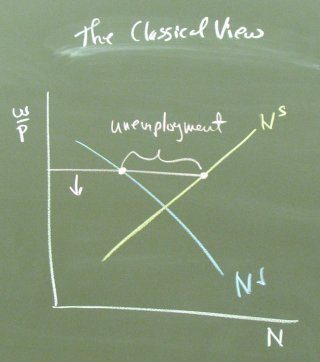

The Classical economists anchored their model on equilibrium in the supply and demand for labor. Unemployment, if it existed, was a temporary phenomenon caused by a real wage rate above the equilibrium value. The wage rate and/or the price level would adjust to eliminate the unemployment.

Keynes demonstrated that a stable equilibrium could exist in a model with no explicit reference to the labor market. The Keynesian equilibrium arose from adjustments in the interest rate, not the real wage rate. If the economy happened to be in equilibrium below full employment, no natural force existed to push the economy toward full employment.

The 25% unemployment rate that prevaled through much of the Great Depression seemed to provide conclusive evidence on the relative merits of the two models.

The major implication of the acceptance of the Keynesian model was that, if equilibrium could be stable with 25% unemployment, then the government should undertake fiscal and monetary policies to move the equilibrium toward full employment.

The data for the 1970's on the Phillips curve handout show that this issue is not settled. By 1980, there were substantial doubts that fiscal and monetary policies could be used to effectively steer the economy.

Posted by bparke at April 25, 2003 05:19 PM