September 04, 2003

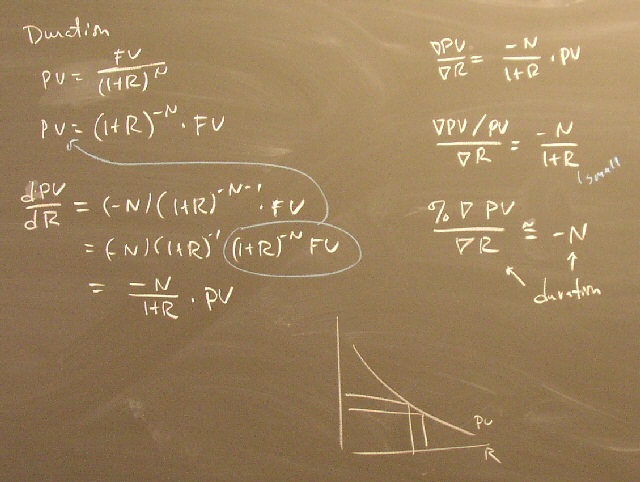

Duration

The duration of a bond (or a portfolio) is defined to be the percentage change in market value caused by a one percentage point change in the interest rate.

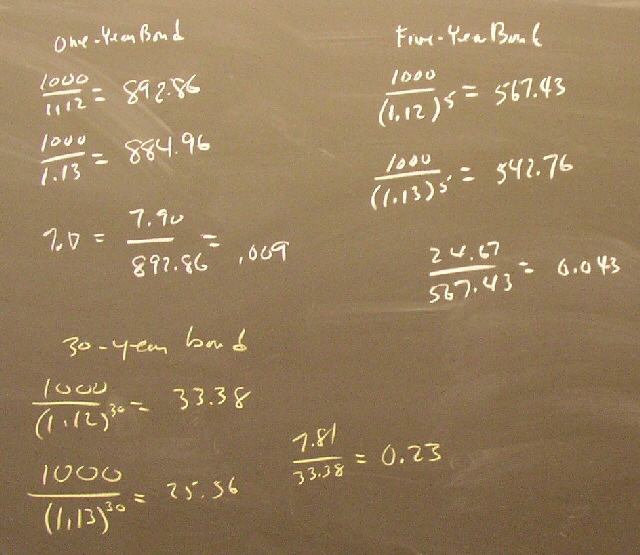

We can use calculus to determine the duration of a pure discount bond.

We can also get some insight into the relation between duration and interest rate risk by running some calculations for pure discount bonds of various maturities and, hence, various durations.