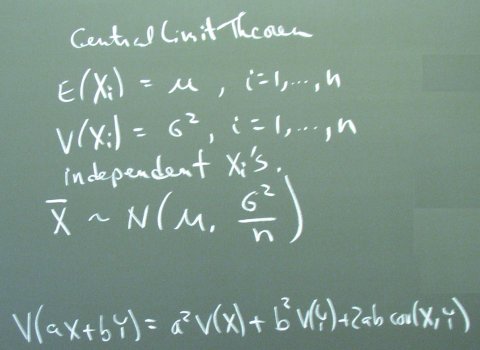

A portfolio of securities lowers risk by exploiting the Central Limit Theorem.

You can also lower risk by looking for negative covariances.