October 28, 2003

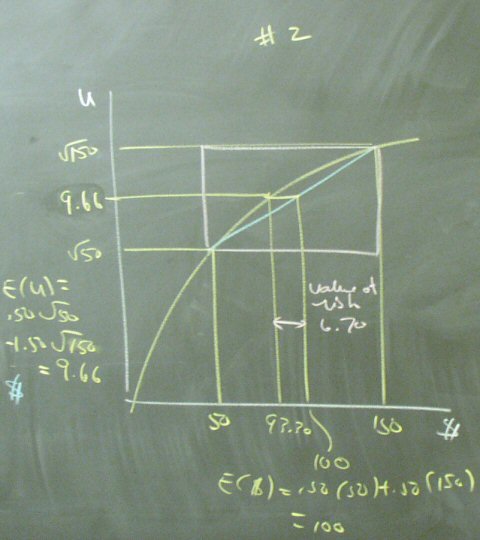

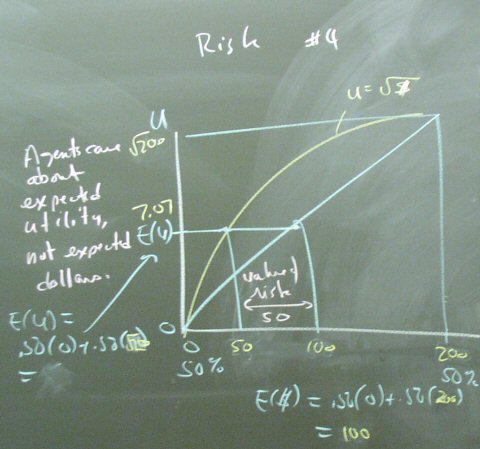

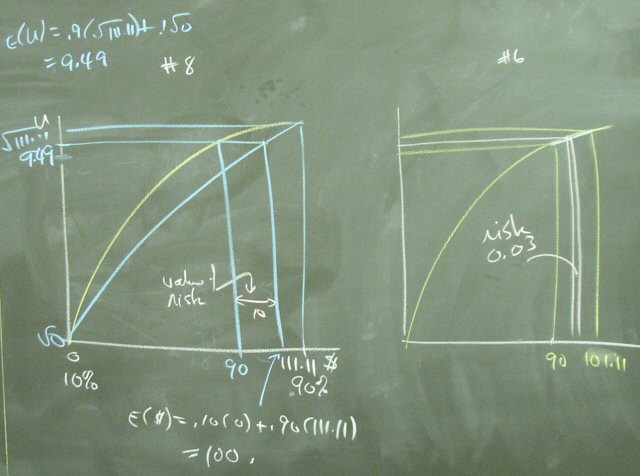

Utility-Based Valuation of Risk

An agents with a curved utility function will place a different value on a risky asset than will an agent with a straight-line utility function if agents care about expected utility, not expected dollars.

We worked through a selection of cases from the handout, getting a feel for how the value of the risk depends on the distance between the good and bad outcomes and the probabilities of those two events.