September 04, 2003

Duration

The duration of a bond (or a portfolio) is defined to be the percentage change in market value caused by a one percentage point change in the interest rate.

We can use calculus to determine the duration of a pure discount bond.

We can also get some insight into the relation between duration and interest rate risk by running some calculations for pure discount bonds of various maturities and, hence, various durations.

Posted by bparke at 10:18 PM

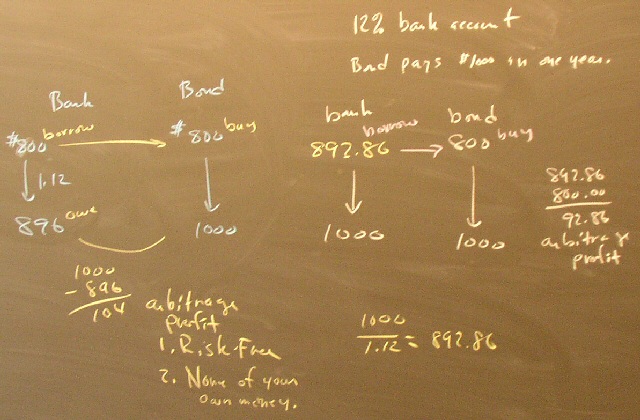

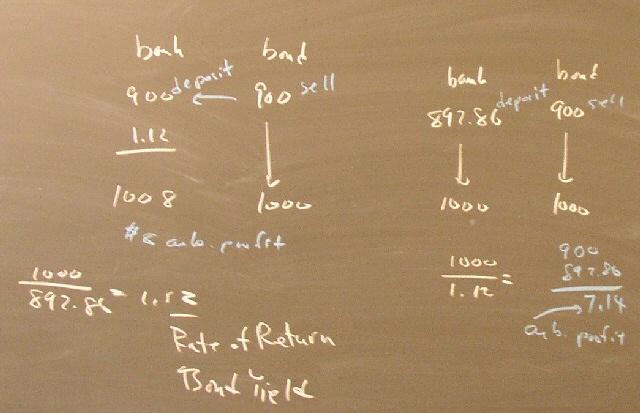

Arbitrage Pricing

Given a bank that loans money and takes deposits at 12%, a bond that pays $1000 in one year must sell for $892.86. Otherwise, a shrewd investor could secure arbitrage profits, which are defined to a risk-free profit gained without putting up any of your own money.

Posted by bparke at 10:10 PM